Rent a Room Relief: A Practical Guide for Homeowners and Airbnb Hosts

Rent a Room Relief Explained - How to Earn £7,500 Tax-Free

In tighter times, many people are opening their doors to lodgers or short‑stay guests. Done right, you get extra income and peace of mind on tax. This guide turns the HMRC rules into plain English so you pay the right tax in the right place and keep more of what you earn.

Quick summary

Tax‑free allowance: Up to £7,500 per tax year if you rent out furnished accommodation in your main home. If income is split (e.g., jointly), the cap is £3,750 each.

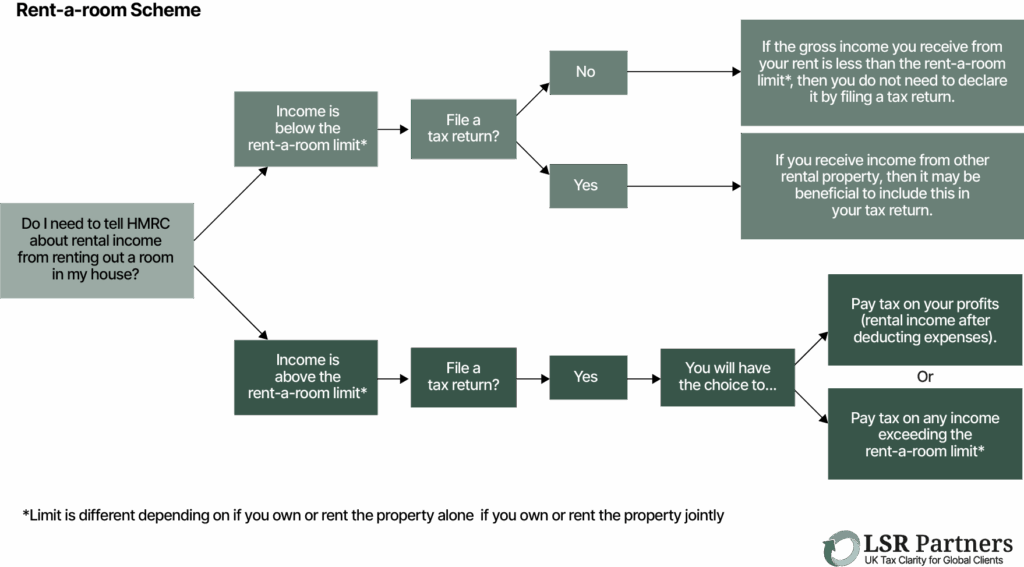

Automatic if under the cap: If your gross receipts are at or below the allowance and you have no other need to file, you typically don’t report anything.

Over the cap? You must report to HMRC. You can elect to use either (a) the £7,500 relief or (b) actual profits after allowable expenses, whichever yields the lower tax.

Short stays (e.g., Airbnb) can qualify where conditions are met (it’s still your main home and a furnished let). Use gross income, not the net after platform fees, when testing the threshold.

You don’t need to own the property you can be a tenant sub‑letting but check your lease/mortgage and local rules.

What is Rent a Room Relief?

Rent a Room Relief is an HMRC scheme that lets you receive up to £7,500 of rent tax‑free each year from letting furnished accommodation in your only or main residence. Where the income is shared (for example, you and a partner), the cap is £3,750 each.

Why consider it now?

Cost‑of‑living pressure: Turn unused space into income without complex compliance.

Flexible work patterns: Hosting a lodger or occasional short‑stay guests can fit around hybrid or travel schedules.

Simple compliance: Stay within the allowance and, in many cases, there’s no return to file just for this income.

Who qualifies?

To qualify, you generally need to:

Let furnished accommodation in your main home (you’re a resident landlord).

Receive gross receipts (before platform fees) at or below £7,500 (or £3,750 each if shared) to benefit automatically.

If receipts exceed the allowance, you report the income and choose the most beneficial method (relief vs. actual profits).

Common misconception: Some hosts mistakenly compare their net Airbnb payouts to £7,500. HMRC looks at gross receipts. Platform fees don’t reduce the test.

Airbnb or short‑term lets while you’re away

Many homeowners prefer not to host while they’re present. In practice, short‑term lets of your main home while you’re away can still fall within Rent a Room Relief where the other conditions are met (it remains your main residence, it is furnished, and you’re treated as a resident landlord for the period). Always consider tenancy agreements, mortgage terms, freeholder/lease rules, and any local restrictions on short‑term letting.

Case in point: We’ve seen people make £5,000 over a couple of weeks away and remain within the annual allowance. The key is ensuring the gross figure is used when testing the limit and that your situation fits the “main home + furnished” requirement.

How to choose: £7,500 relief vs. actual expenses

If your gross receipts exceed the allowance, you must declare the income and decide how to be taxed:

Option A: Elect the £7,500 relief

You’re taxed on gross receipts minus £7,500 (not on profits after expenses).

You can’t deduct actual expenses on top.

Option B: Use normal property income rules

You report rental income minus allowable expenses (e.g., a fair share of utilities, repairs, insurance related to letting the room).

This can be better if your costs are high relative to receipts.

Tip: Keep clean records of all receipts and platform statements. If using Airbnb or similar, export the gross transaction history for each tax year.

Do you have to file a tax return?

No, if: Your gross Rent a Room receipts are at or below the allowance and you have no other reason to file. The relief operates automatically.

Yes, if: Your gross receipts exceed the allowance or you already file for other reasons (e.g., foreign income, self‑employment). In that case, make the annual choice between the Rent a Room election and the actual‑expense route.

Practical guardrails

Lease & mortgage: Confirm you’re permitted to host or sub‑let.

Insurance: Tell your home insurer about hosting, ensure liability cover.

Safety & compliance: Gas safety, smoke alarms, and local rules still matter.

Record‑keeping: Keep gross receipts, dates, and any expenses.

Joint owners/hosts: Remember the £3,750 each split when the income is shared.

FAQs

Does Rent a Room Relief require me to own the property? No. You can be a tenant and sub‑let (where your agreement allows it). The test is about your main home and furnished accommodation.

Can I deduct Airbnb fees to stay under £7,500? No. HMRC tests the gross receipts before fees.

If my receipts exceed £7,500, do I lose the relief? You don’t lose it, but you must file and then choose between the Rent a Room basis or normal property income rules.

What if I only rent while I’m away? Short‑term lets can still qualify if it remains your main residence and is furnished. Check contracts and local rules first.

Do I need to register with HMRC before hosting? Not if you’re within the allowance and have no other filing requirement. If you expect to exceed it, plan your record‑keeping and filing.

Will this affect Capital Gains Tax on my home? Renting rooms generally doesn’t jeopardise your core Private Residence Relief, but edge cases exist (e.g., exclusive business use). Get tailored advice.

Disclaimer

This article is for general information only. Tax rules can change and your circumstances are unique. Get personalised advice before acting.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behaviour or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.